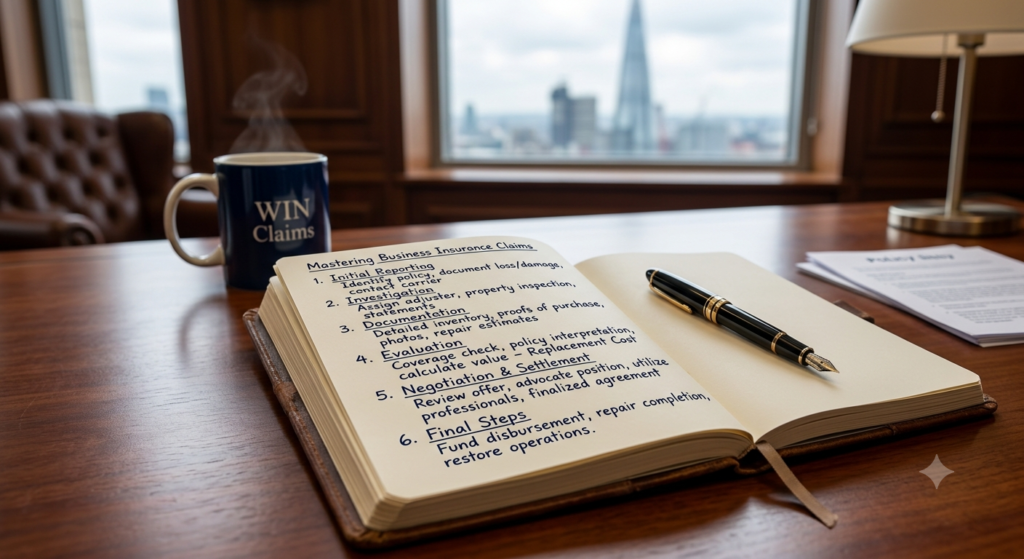

7 Proven Strategies to Win Business Insurance Claims in 2026

Navigating the Business Insurance Claims process is a critical hurdle for any company. Successfully handling this path determines whether your organization recovers quickly or faces devastating financial consequences. In this guide, we provide a strategic approach to managing these filings effectively in 2026.

Table of Content

- Understanding the Claim Lifecycle

- Documentation Best Practices

- Navigating the 2026 Insurance Landscape

- Maximizing Your Settlement

- Strategic Communication with Adjusters

- Avoiding Common Pitfalls

- Handling Claim Denials

- Business Continuity Planning

Why Mastering This Process is Essential

The financial stability of your enterprise depends on your ability to process claims accurately. By understanding the policy language and the adjuster’s evaluation criteria, you turn an administrative burden into a strategic victory. When an incident occurs, time is of the essence; the sooner you establish a professional dialogue with your provider, the higher your chances of a favorable outcome.

1. Documentation: The Foundation

When submitting formal requests for coverage, documentation is your strongest asset. Maintain a digital archive of all assets, repair receipts, and communication logs. Without clear proof of loss, adjusters may default to minimum payouts. For more insights on record-keeping, visit the Insurance Information Institute.

2. Navigating the 2026 Landscape

The 2026 market is more competitive than ever. Insurance carriers are increasingly using AI and advanced algorithms to flag discrepancies in claims. Ensure your submissions are audited by a professional or internal risk manager before they reach the carrier. You can learn more about regulatory updates at the NAIC website.

3. Maximizing Settlement Values

To successfully resolve a claim, you must distinguish between Actual Cash Value and Replacement Cost. Actual Cash Value takes depreciation into account, which often leads to lower payouts. Always push for Replacement Cost to ensure your business is restored to its original operational capacity without significant out-of-pocket costs.

4. Strategic Communication

Always remain professional and fact-driven. Remember that an adjuster is managing multiple files simultaneously; your organized, data-heavy submission will naturally move to the top of their priority list. Avoid emotional appeals and stick to the contractual obligations outlined in your policy documents. Clear, written communication is essential for creating a paper trail.

5. Avoiding Common Pitfalls

Many policyholders lose money by failing to update their coverage limits. If your business has expanded in the last year, your old policy may not cover the current value of your inventory or infrastructure. Regularly review your General Liability Insurance to ensure you have adequate protection.

6. Handling Claim Denials

If your claim is initially denied, do not panic. Denials are often the first step in a negotiation process, not the final word. Request a written explanation of the denial, referencing the specific policy clause used to justify it. Often, this reveals an interpretation that can be challenged with additional documentation or expert testimony. Persistence and precision are your best tools here.

7. The Role of Business Continuity Planning

A major loss can halt operations entirely. Business Continuity Planning is your roadmap for survival while your insurance claim is being processed. By having a pre-drafted plan, you demonstrate to the insurance company that you are managing your “Extra Expenses” prudently. This proactively strengthens your claim by showing that you have mitigated further revenue loss through strategic action.

8. Professional Advocacy

If you find yourself stuck, professional help is vital. Public adjusters or legal counsel specializing in commercial insurance can provide the leverage needed to negotiate with large carriers. They understand the “insurance speak” that often confuses business owners and can identify clauses that you might have missed during the initial contract review.

9. Analyzing Policy Language: The Art of Contractual Interpretation

Beyond the surface-level documentation, the true battleground for any insurance claim lies in the precise interpretation of your policy’s language. Many business owners make the mistake of accepting an adjuster’s initial explanation of a policy exclusion without questioning the underlying legal logic. Insurance contracts are complex, legalistic documents designed to protect the carrier, but they are subject to strict rules of construction. Understanding how to interpret these nuances is the ultimate skill in managing complex Business Insurance Claims.

When you receive a denial or a limited settlement offer, you must demand the specific policy endorsement or clause being cited. Often, adjusters will point to “wear and tear” exclusions or “maintenance” clauses to deflect responsibility for property damage. However, if you can provide professional reports—such as forensic engineering studies or climate data—that demonstrate the loss was triggered by an external, sudden, and accidental event, you can effectively override these boilerplate exclusions. This requires a forensic approach to reading your policy; you are not looking for what the policy does not cover, but rather for the specific definitions that define the scope of your covered perils.

Furthermore, it is critical to understand the concept of “ambiguity.” In many jurisdictions, courts have established that if a policy provision is subject to multiple reasonable interpretations, the court should adopt the interpretation that favors the policyholder. This is a powerful leverage point. If your carrier is taking a hyper-restrictive view of a vague clause, you have the right to challenge that interpretation by presenting legal precedents or past case studies where similar language was interpreted in favor of the insured. You are essentially shifting the conversation from a casual discussion about “what is covered” to a formal legal argument regarding the scope of your contractual rights.

Lastly, you must consider the “Duty to Defend” versus the “Duty to Indemnify.” In many liability claims, your insurer’s obligation to provide a legal defense is much broader than their obligation to pay a final judgment. By forcing the insurance company to acknowledge their broader duty to defend, you often trigger a more favorable settlement environment, as the carrier becomes motivated to resolve the claim quickly to mitigate their own ongoing legal defense costs. Mastering these contractual dynamics turns you from a vulnerable claimant into a sophisticated negotiator who understands exactly how to hold the insurance carrier accountable to the promises made in your original policy agreement.