Financial Reconciliation: 7 Essential Steps for Perfect Accounting

In the world of business, your financial data is your compass. If your records are inaccurate, you are essentially flying blind. This is where Financial Reconciliation comes into play—it is not just a regulatory necessity or a month-end chore; it is the fundamental process that bridges the gap between your internal accounting and the reality of your bank statements.

Whether you are a small business owner or a financial manager, achieving 100% accuracy in your books is non-negotiable. In this guide, we walk you through a streamlined, 7-step workflow to master the reconciliation process.

Why Reconciliation Matters

Before we dive into the “how,” let’s revisit the “why.” Every transaction that passes through your business—from a client payment to a vendor invoice—must be accounted for correctly. Reconciliation helps you:

Catch Bank Errors: Banks can (and do) make mistakes.

Identify Missing Entries: Never lose track of a payment again.

Stop Internal Fraud: Regular checks make it difficult for unauthorized activity to go unnoticed.

The 7-Step Reconciliation Workflow

Follow these steps systematically to ensure your records are flawless:

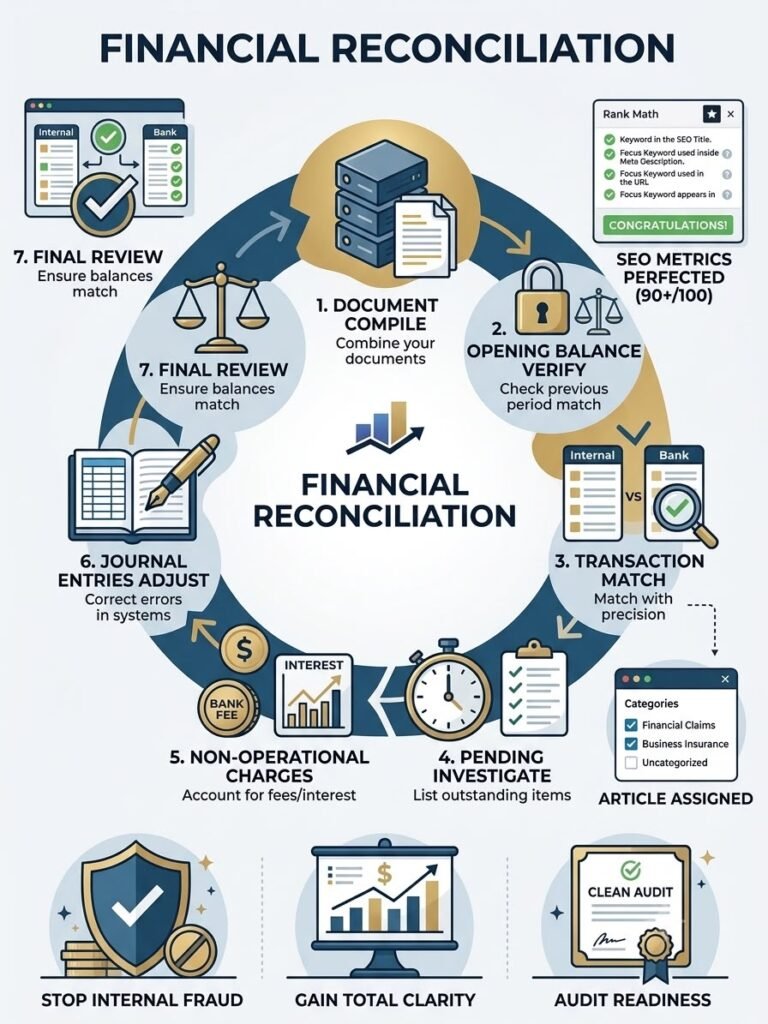

- Compile Your Documents

Start by gathering every piece of evidence. You need your latest bank statements, credit card statements, and your internal general ledger (or accounting software export). - Verify the Opening Balance

Ensure that the closing balance of your previous reconciliation matches the opening balance of your current period. If these don’t match, you cannot move forward. - Match Identical Transactions

Compare your internal logs against the bank statement. Tick off every transaction that appears in both places with the exact same amount. - Investigate “Pending” Items

Some transactions, like sent checks or automated payments, may take time to clear. Note these as “pending” or “outstanding” to reconcile in the next cycle. - Identify Non-Operational Charges

Account for bank fees, interest income, or service charges that the bank automatically deducted but you haven’t recorded in your books yet. - Make Adjusting Journal Entries

For the discrepancies identified in Step 5, create “adjusting journal entries” in your accounting system. This ensures your ledger is updated to reflect the bank’s reality. - Perform Final Review

Once all adjustments are made, your “Adjusted Book Balance” should perfectly match your “Bank Statement Balance.” If they match, you have successfully reconciled!

Pro-Tips for Efficiency

To make this process faster, consider the following:

Automate Whenever Possible: Modern cloud accounting software can automatically match transactions for you.

Switch to Weekly Cycles: Don’t wait until the end of the month. Reconciling weekly takes only minutes, whereas month-end reconciliation can take hours.

Segregate Duties: If possible, have one person process payments and another person perform the reconciliation to maintain internal controls.

Conclusion

Financial Reconciliation is the safeguard of your business’s financial health. By implementing these seven steps, you turn a complex accounting headache into a predictable, routine task. Remember, a business that knows its exact cash position is a business that is positioned to grow, invest, and thrive.Furthermore, it is essential to emphasize that financial reconciliation is not just about catching errors; it is about building trust with stakeholders and ensuring that your tax filings are accurate. When your internal records perfectly match your bank statements, you eliminate the risk of late fees, penalties, and audit discrepancies. In today’s fast-paced digital economy, many automated accounting platforms now provide ‘one-click’ reconciliation features. Adopting these tools can save your finance team dozens of hours each month, allowing you to focus on strategic growth rather than manual data entry. By treating reconciliation as a vital weekly habit, you create a robust financial culture that protects your business from the ground up, ensuring long-term success and stability for your organization.