After a car accident, getting your vehicle repaired and your medical bills paid is a top priority. However, one question always looms large: how long does a car insurance claim take to settle? The truth is, there is no single nationwide deadline. The timeline for a payout depends heavily on the complexity of the accident, the responsiveness of the parties involved, and—most importantly—the specific state laws where the accident occurred.

Thank you for reading this post, don't forget to subscribe!While some simple property damage claims can wrap up in a matter of days, complex injury claims can drag on for months or even years. This comprehensive guide breaks down the legal time limits insurance companies must follow state-by-state in 2026, and what you can do to accelerate the process.

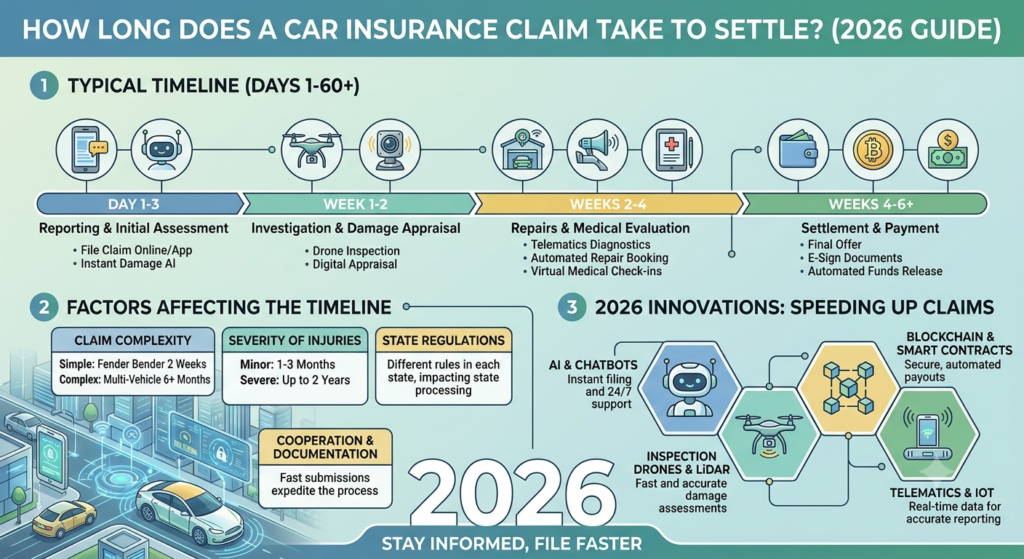

The Standard Claim Timeline: A Step-by-Step Overview

Before examining state-specific legal limits, it helps to understand the standard lifecycle of an auto insurance claim. Insurance adjusters generally follow a structured timeline to investigate liability and evaluate damages:

- Acknowledgment Phase (10 to 15 Days): Once you file, the insurer must officially acknowledge your claim and provide necessary forms.

- Investigation Phase (15 to 30 Days): The adjuster reviews police reports, inspects vehicle damage, and interviews witnesses to determine fault.

- Approval or Denial (15 to 40 Days): After completing the investigation, the insurer must legally notify you whether they accept or deny the claim.

- Payment Phase (5 to 10 Days): Once a settlement agreement is signed, state laws dictate how quickly the check must be issued.

State-by-State Breakdown: Legal Deadlines for Claim Settlements

Most states regulate insurance companies through “Unfair Claims Settlement Practices Acts,” forcing insurers to act within specific windowframes. Below is the 2026 update on how long insurers have to accept or deny a claim after receiving proof of loss across key states:

States with Strict 30-Day Windows

These states have consumer-friendly regulations that force insurance adjusters to make an official decision within 30 days of receiving your completed documentation:

- California: 40 days to accept or deny a claim; payment must follow within 30 days of settlement approval.

- Texas: 15 business days to acknowledge, 15 business days to accept/deny, and 5 business days to issue payment after approval.

- Florida: Insurers have 14 days to acknowledge, 90 days to pay or deny personal injury protection (PIP) and property claims under strict 2026 guidelines.

- New York: 15 business days to inspect and determine liability; payment must be made within 5 business days of reaching an agreement.

States Operating Under “Reasonable Time” Statutes

A few states do not explicitly state a fixed number of days in their statutes. Instead, they require actions to be taken within a “reasonable time.” If an insurer drags their feet without a valid legal reason, they can be sued for bad faith.

- Pennsylvania: Requires acknowledgment within 10 days and a decision within 30 days. If a decision cannot be made, they must send a written update every 45 days.

- Ohio: 15 days to acknowledge and 21 days to decide after proof of loss is submitted.

For a deeper look into your rights or to report an insurer that is violating these timelines, you can find your local authority through the National Association of Insurance Commissioners (NAIC) consumer directory.

Why is Your Car Insurance Claim Delayed?

If your claim is taking longer than the state averages, it is usually driven by specific roadblocks. Understanding these variables can help you figure out if you need to escalate the situation:

- Disputed Liability: If the other driver’s insurance denies fault or claims you are partially responsible, the investigation halts until further evidence is found. If this happens, knowing how to appeal an auto insurance claim denial is an essential next step.

- Severe Injuries and MMI: You should never settle an injury claim until you reach Maximum Medical Improvement (MMI). Settling too early means you cannot ask for more money if you need future surgeries.

- Total Loss Calculations: Determining the actual cash value of a totaled vehicle requires extra market research, which inherently lengthens the timeline.

How to Speed Up Your Auto Insurance Settlement

While you cannot control the insurance company’s internal bureaucratic speed, you can prevent them from using your own mistakes as an excuse to delay your payout. Follow these proactive steps:

- Submit an Air-Tight Evidence Package: Do not submit documents piece by piece. Send photos, police reports, and repair estimates all at once. This establishes an official “Proof of Loss” date, triggering the state’s legal countdown clock.

- Follow Up in Writing: Keep a detailed log of every phone call, but always send a follow-up email confirming what was discussed. Documenting communication builds a foundation if you ever need to file a bad-faith insurance complaint.

- Understand Your Policy Limits: Make sure you know what you are legally entitled to. Reviewing the basic minimum car insurance requirements by state will give you context on the coverage limits the other driver might be working with.

Final Checklist: Tracking Your Settlement Timeline

Are you currently waiting on an insurance payout? Use this quick checklist to ensure your claim is moving forward legally:

- [ ] Have I received an official claim number and a designated adjuster’s contact info?

- [ ] Did I submit a formal, written “Proof of Loss” to officially start the state’s legal clock?

- [ ] Am I documenting every delay or extension request sent by the insurance company?

- [ ] If the insurer is acting in bad faith, have I consulted a legal professional or my state’s insurance commissioner?

Conclusion

So, how long does a car insurance claim take to settle? For straightforward vehicle damage, expect 2 to 4 weeks. For bodily injury, expect anywhere from several months to a year. Stay organized, understand your state’s strict legal deadlines, and never let an insurance adjuster pressure you into a lowball settlement just because the process is taking time.

Disclaimer: Timeframes and statutory deadlines can change based on legislative amendments and individual policy endorsements. For specific legal guidance regarding a delayed settlement, always consult with a licensed attorney in your jurisdiction.