How to Check If a Financial Firm Is FCA Authorised in the UK: The Definitive 2026 Guide

The UK financial sector is one of the most vibrant and strictly regulated markets in the world. However, its sheer size and reputation also make it a primary target for sophisticated financial criminals, identity thieves, and offshore scammers looking to exploit everyday investors. Before you hand over your hard-earned money, deposit savings, or sign an investment contract with any online platform, broker, or loan provider, there is one non-negotiable, safety-critical step you must take: you must check if the firm is authorised by the Financial Conduct Authority (FCA). Knowing how to accurately execute this verification can be the absolute line of defense between protecting your net worth and losing your entire life savings to devastating financial fraud.

Thank you for reading this post, don't forget to subscribe!In this exhaustive, industry-grade guide, we will walk you through the structural realities of UK financial regulation. You will learn how to properly check an FCA authorised firm in the UK, identify the complex tricks used by “clone firms,” evaluate specific regulatory permissions, and understand the critical safety nets designed to rescue consumers when things go wrong.

Why Verifying FCA Authorization is a Legal Safety Net

Operating a financial services business in the United Kingdom without explicit authorization or exemption from the FCA is not just a breach of guidelines—it is a serious criminal offense under the Financial Services and Markets Act 2000. The regulatory framework established by the UK government is built entirely to protect consumers, maintain market integrity, and promote healthy competition. When you choose to deal exclusively with an authorised firm, you are instantly granted a legally backed safety net that unregulated entities simply cannot duplicate.

The Financial Ombudsman Service (FOS) Shield

If you have a dispute with an authorised financial firm regarding hidden fees, misleading investment advice, or administrative errors, you don’t have to hire an expensive lawyer. You have the right to escalate your complaint to the Financial Ombudsman Service (FOS). The FOS is a completely free, independent body that reviews disputes and has the legal power to order authorised firms to pay compensation to consumers if they have been treated unfairly.

The Financial Services Compensation Scheme (FSCS) Protection

What happens if the financial firm you are investing with goes completely bankrupt? If the firm is officially authorised by the FCA, your capital is protected by the Financial Services Compensation Scheme (FSCS). Under current UK regulations, the FSCS covers up to £85,000 per person, per eligible institution for banking deposits and investment products. If you bypass the check for an FCA authorised firm in the UK and invest with an unregulated entity, you forfeit these multi-layered protections completely. If that entity disappears or collapses, no government body or scheme can recover your stolen assets.

Authorised vs. Registered: Understanding the Crucial Difference

When searching the Financial Services Register, many consumers mistakenly assume that any company appearing in the database is fully backed by the FCA. This is a dangerous misconception. The register includes entities categorized under completely different levels of regulatory oversight:

- FCA Authorised Firms: These companies have undergone rigorous, months-long background checks, capital adequacy assessments, and operational scrutiny by regulators. They are fully permitted to conduct specific regulated activities and offer full consumer protections (FOS and FSCS eligibility).

- FCA Registered Firms: Certain businesses, such as standard payment service providers, e-money institutions, or mutual societies, are only required to be “registered” rather than fully authorised. While they are on the register, they may not offer the same level of statutory compensation schemes if they go out of business.

- Appointed Representatives (AR): These are firms or individuals that are not directly authorised by the FCA but carry out regulated activities under the full legal responsibility of an authorised firm (known as the “Principal”). If you deal with an AR, you must verify that their Principal firm is active and in good standing.

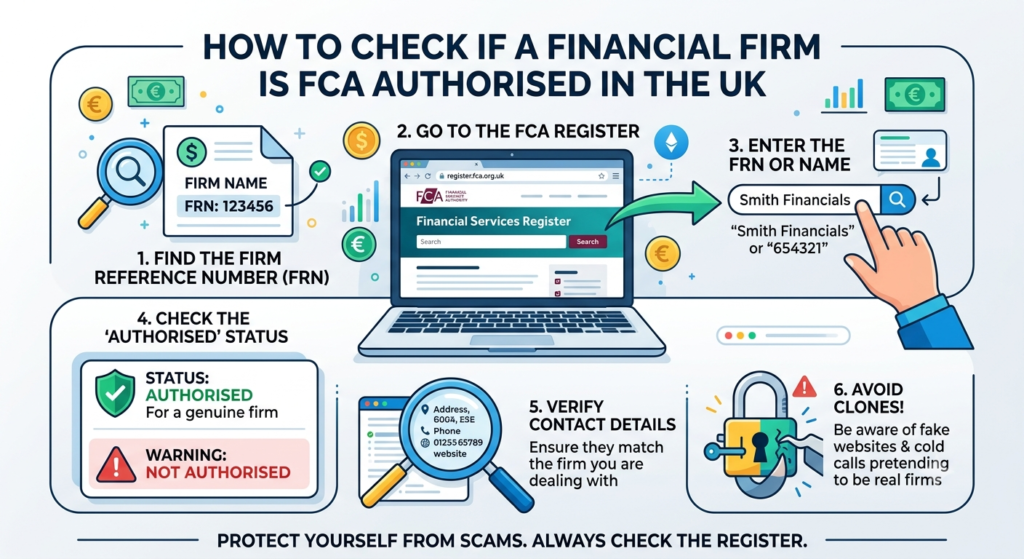

Step-by-Step: How to Check an FCA Authorised Firm in the UK

The only official, legal, and foolproof method to verify a company’s regulatory status is by using the official Financial Services Register portal. Do not trust digital certificates displayed on a company’s own website, as these are routinely forged. Follow this precise, step-by-step verification protocol:

- Access the Official Register Directly: Open your browser and navigate directly to the official government portal via the Financial Conduct Authority (FCA) home page and click through to the Financial Services Register. Avoid searching for the register on generic search engines, as scammers sometimes buy Google Ads to point victims toward fake, cloned versions of the register itself.

- Search Using the Firm Reference Number (FRN): Every single authorised entity is assigned a unique 6 or 7-digit Firm Reference Number (FRN). Searching by FRN is infinitely safer than searching by company name, because fraudulent companies intentionally name themselves almost identically to legitimate corporate entities to confuse the public.

- Analyze the Active Status Label: Once the firm’s profile loads, look at the top status bar. It must explicitly state “Authorised” or “Active”. If the status reads “No longer authorised,” “Cancelled,” or “Suspended,” terminate all professional communications and transactions immediately.

- Cross-Reference the Permitted Regulated Activities: Scroll down to the “Permissions” and “Regulated Activities” tab. A financial firm is strictly bound to the specific permissions granted to them. For example, a company might be legally authorised to provide vehicle financing or standard insurance broking, but completely unauthorized to manage investment funds, trade cryptocurrency, or offer retirement pensions. Ensure the exact service they are attempting to sell you matches their legal permissions.

- Verify the Contact Details Line by Line: This is where most victims get caught out. Scammers will use a real firm’s name but provide their own phone numbers and email addresses. You must check that the telephone number, official website URL, and email domain listed on the FCA Register match the exact contact details of the person you are communicating with.

Beware of Clone Firms: The Ultimate Scammer Trick

As security measures improve, modern financial scammers have turned heavily to a highly deceptive tactic known as a “Clone Firm.” In a clone firm scam, the criminals do not attempt to create a fake company from scratch. Instead, they find a real, perfectly legitimate, fully FCA-authorised firm that keeps a low digital profile. The scammers then copy the real firm’s FRN, corporate registration details, and executive names, and present them to potential victims as their own.

They will set up professional-looking websites using almost identical domains (e.g., changing `.co.uk` to `.net` or adding a minor hyphen) and send out slick brochures. When a cautious investor checks the FCA register, everything looks perfect because the real firm is indeed authorised.

To completely isolate yourself from clone firm risks, implement the “Call Back” rule: Never use the phone numbers, links, or contact forms provided in an incoming email, text message, or cold call. Instead, go to the official FCA register, copy the phone number listed under the firm’s profile, and call the company back through that specific number to verify if the employee contacting you actually works there.

Furthermore, you should actively check the FCA Warning List before making any decisions. This warning list is an updated index of unauthorized entities, suspected clones, and offshore platforms that the FCA has actively flagged as high-risk or fraudulent operations targeting UK residents.

What Happens If You Lose Money to an Unauthorised Firm?

If you discover that a company is completely unregulated or unauthorized after you have already transferred funds, made a deposit, or paid upfront fees, the reality of recovering your capital is incredibly grim. Unlike dealing with regulated credit cards, banking claims, or standard motor coverage where you can systematically evaluate how to check if you have a valid claim, dealing with an unauthorised scam puts you entirely outside the safety net of civilized financial architecture.

Because the FSCS cannot intervene in scams operated by unregulated entities, your legal remedies are severely limited. Your immediate actions should include:

- Report to Action Fraud: Report the incident to Action Fraud (the UK’s national fraud and cybercrime reporting center) to initiate a police tracking file.

- Notify Your Bank Instantly: Inform your bank’s fraud department immediately. If the transfer was made recently, they may be able to freeze the funds before they exit the UK banking system via a Contingent Reimbursement Model (CRM) trigger.

- Report to the FCA: Submit a report directly to the FCA consumer helpline so they can add the entity to their public warning list, preventing others from falling victim.

Ultimately, preventative checking is your only true protection. Spending five minutes to check an FCA authorised firm in the UK before sending money is the single most valuable financial habit you can build to defend your wealth.

Final Regulatory Checklist Before Depositing Funds

Before you invest, transfer money, or buy a financial package, ensure you can check off every single requirement below:

- [ ] I have personally opened the Financial Services Register website by typing the address manually.

- [ ] I have verified that the firm’s regulatory status explicitly says “Authorised”.

- [ ] I have matched the Firm Reference Number (FRN) exactly with all contracts provided.

- [ ] I have called the firm using the phone number listed on the FCA register to confirm the offer is genuine.

- [ ] I have confirmed the firm has explicit legal permissions for the exact type of investment or service being offered.

- [ ] I have searched the FCA Warning List and confirmed there are no active consumer alerts against this name or its variations.

Conclusion

Protecting your financial future requires relentless, uncompromising verification. A legitimate financial firm will always welcome your regulatory due diligence and understand why you are verifying their credentials. It takes less than two minutes to check an FCA authorised firm in the UK, yet ignoring this simple step is the leading reason individuals lose their life savings to clones and unregulated offshore platforms. Treat regulatory authorization as your definitive green light—if a firm isn’t on the official register with active permissions, walk away immediately, no matter how attractive the returns appear.

Disclaimer: While checking FCA authorization drastically lowers your operational risk and protects you against outright scams, it does not guarantee investment returns, shield against normal market volatility, or substitute for independent financial planning. Always perform full commercial due diligence before risking capital.