Driving without insurance isn’t just a financial gamble; in almost every U.S. state, it is a serious legal violation. However, buying “just enough” coverage to satisfy the law can be confusing. Every state sets its own mandates for financial responsibility, and navigating these legal limits is crucial to keeping your registration valid and protecting your assets if an accident occurs.

Thank you for reading this post, don't forget to subscribe!This comprehensive guide breaks down the statutory minimum car insurance requirements across the United States for 2026, explains the shorthand numbers you see on policies, and highlights the hidden risks of relying solely on minimum coverage.

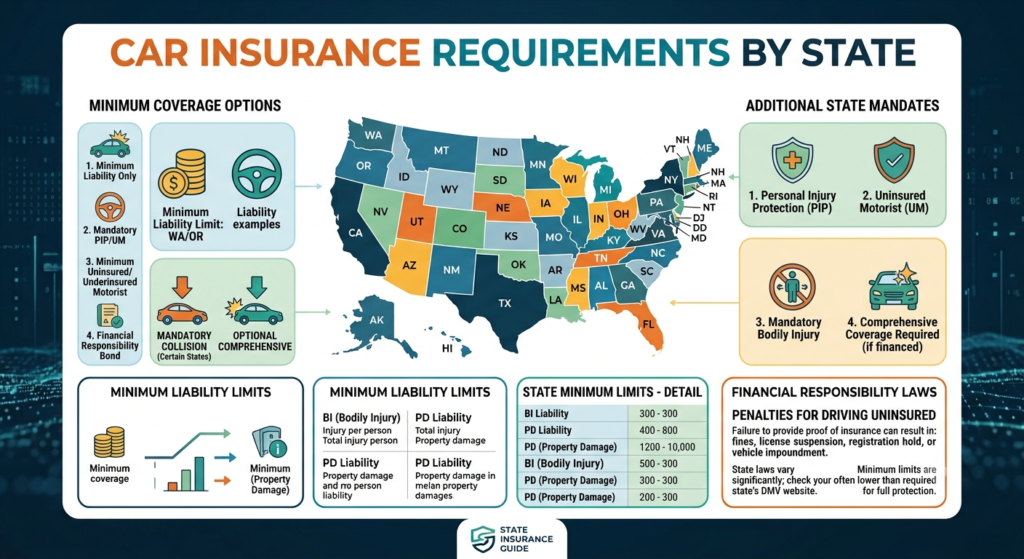

Understanding the Numbers: What Does 25/50/25 Mean?

When reviewing state insurance mandates, you will frequently see requirements expressed as a series of three numbers separated by slashes (e.g., 25/50/25). This is the shorthand for **split-limit liability coverage**, and understanding it is vital before purchasing a policy.

- First Number (Bodily Injury Per Person): The maximum amount your insurer will pay for medical expenses or injuries to a single person in an accident you cause.

- Second Number (Bodily Injury Per Accident): The total cap your insurer will pay for all injured parties combined in a single accident.

- Third Number (Property Damage Liability): The maximum amount paid to repair or replace another person’s property, such as their vehicle, fence, or storefront.

For example, if your state requires 25/50/25, your insurance will cover up to $25,000 for one person’s injuries, up to $50,000 total for everyone hurt in the crash, and up to $25,000 for any property damage you cause.

2026 State-by-State Minimum Auto Insurance Requirements

While most states utilize the split-limit system outlined above, specific limits vary dramatically. Below is the updated breakdown of the mandatory liability limits across key jurisdictions:

High-Limit States (Stricter Mandates)

States with higher minimums force drivers to carry more protection upfront, reducing the immediate risk of personal lawsuits after minor collisions.

- Alaska: 50/100/25

- Maine: 50/100/25

- Maryland: 30/60/15

- North Carolina: 30/60/25

- Texas: 30/60/25

Standard-Limit States (The National Average)

The majority of states fall into this cluster, requiring balanced numbers that have remained steady heading into 2026.

- California: 15/30/5 (Note: California’s property damage minimum remains exceptionally low at $5,000)

- Georgia: 25/50/25

- New York: 25/50/10 (Also mandates $50,000 for wrongful death per person)

- Ohio: 25/50/25

- Pennsylvania: 15/30/5

The No-Fault Exceptions (PIP States)

Several states operate under a **no-fault insurance system**, requiring drivers to carry Personal Injury Protection (PIP). In these states, your own insurer pays for your medical bills regardless of who caused the accident.

- Florida: 10/20/10 split liability alongside a mandatory $10,000 in PIP coverage.

- Michigan: Requires unique No-Fault Personal Injury Protection, which allows drivers to choose varying levels of medical coverage, including unlimited lifetime medical benefits.

- New Jersey: Standard policies require 25/50/25 plus $15,000 PIP, though basic lower-limit alternatives exist for low-income drivers.

For an official, legally binding directory of local updates, you can consult the National Association of Insurance Commissioners (NAIC) map to link directly to your specific State Department of Insurance.

The Severe Legal Risks of Driving Uninsured

Choosing to bypass your state’s minimum requirements is a costly mistake. Law enforcement and state DMVs utilize automated registration cross-checks with insurance databases to catch lapses instantly.

If caught driving without insurance, you face severe penalties including:

- Heavy Fines: Ranging from a few hundred to several thousand dollars depending on prior offenses.

- License and Registration Suspension: Reinstatement often requires a hefty fee and filing an SR-22 form.

- The SR-22 Requirement: A certificate of financial responsibility that your insurer files with the state proving you carry minimum coverage. This tags you as a high-risk motorist, exponentially raising your rates. If you find yourself in this situation, it is best to review high-risk car insurance options immediately to find specialized carriers.

Why State Minimums Are Simply Not Enough

The biggest misconception among buyers is that “state minimum” means “fully protected.” State minimums are designed to protect the other driver, not you, and they are dangerously low compared to modern economic realities.

Consider this scenario: You live in California, carrying the minimum $5,000 property damage coverage. You accidentally rear-end a brand new $60,000 electric vehicle, totaling it. Your insurance company will write a check for $5,000 to the other driver—and walk away. You are personally on the hook for the remaining $55,000 out-of-pocket.

If you cannot pay, the injured party can sue you, resulting in garnished wages or liens placed on your home. Furthermore, state minimums include zero coverage for your own vehicle if it is damaged or totaled. To truly safeguard your finances, you must understand how optional coverages protect your own asset gap, which is why evaluating how to check if you have a valid claim or asset protection is so critical.

Final Checklist for Purchasing Auto Insurance

Before you sign a basic, state-minimum policy, run through this final checklist to assess your exposure:

- [ ] Does my property damage limit cover the average cost of a new car on the road today ($40,000+)?

- [ ] If I injure multiple people, will my bodily injury per-accident limit protect my personal savings from a lawsuit?

- [ ] Does my state require additional Uninsured/Underinsured Motorist (UM/UIM) coverage to protect me from hit-and-runs?

- [ ] Have I shopped around independently instead of accepting dealership-bundled or low-tier, non-standard options?

Conclusion

Meeting your state’s minimum car insurance requirements keeps you legal, but it rarely keeps you safe from financial ruin. Treat insurance as a shield for your net worth. If you have assets to protect, consider raising your limits to 100/300/100—the slight increase in monthly premium is almost always worth the peace of mind.

Disclaimer: Insurance statutes and mandates are subject to frequent legislative updates. Always verify current minimum obligations directly with your state’s Department of Motor Vehicles or a licensed insurance professional before purchasing a policy.