How To Check If I Have A Compensation Claim

Many people suffer losses—financial, personal, or physical—and simply absorb the cost, assuming that the misfortune is just “bad luck.” However, there is a distinct, legally recognized difference between an unfortunate accident and a compensable claim. Knowing how to evaluate your situation can be the difference between bearing a heavy financial burden alone and receiving the restitution you are entitled to.

Thank you for reading this post, don't forget to subscribe!Identifying the Core Elements of a Claim

Not every bad experience results in a legal claim. To determine if you have a viable path to compensation, you must first identify if your situation meets the fundamental criteria for liability.

The Three Pillars of a Valid Claim

- Duty of Care: The party you are holding responsible must have had a legal obligation to act safely or reasonably toward you.

- Breach of Duty: That party failed to meet their obligation, either through action or negligence.

- Causation and Damages: The breach of duty directly caused an injury or financial loss that is quantifiable in monetary terms.

If you cannot connect the negligence to a specific, measurable loss, the path to a successful claim becomes significantly harder.

Assessing Your Financial and Personal Damages

Compensation is intended to make you “whole” again, not to provide a windfall. To check if you have a claim worth pursuing, you must list your damages:

- Medical Expenses: Past and future bills for treatment, surgery, physical therapy, or medications related to the incident.

- Lost Wages: Income lost because you were unable to work, including potential future loss of earning capacity.

- Property Damage: Costs to repair or replace vehicles, equipment, or personal belongings.

- Pain and Suffering: Non-economic damages related to physical pain, emotional distress, or loss of enjoyment of life.

Note: If your damages are negligible or purely speculative, legal counsel or insurers may advise that the costs of pursuing a claim exceed the potential payout. Always conduct a cost-benefit analysis before proceeding.

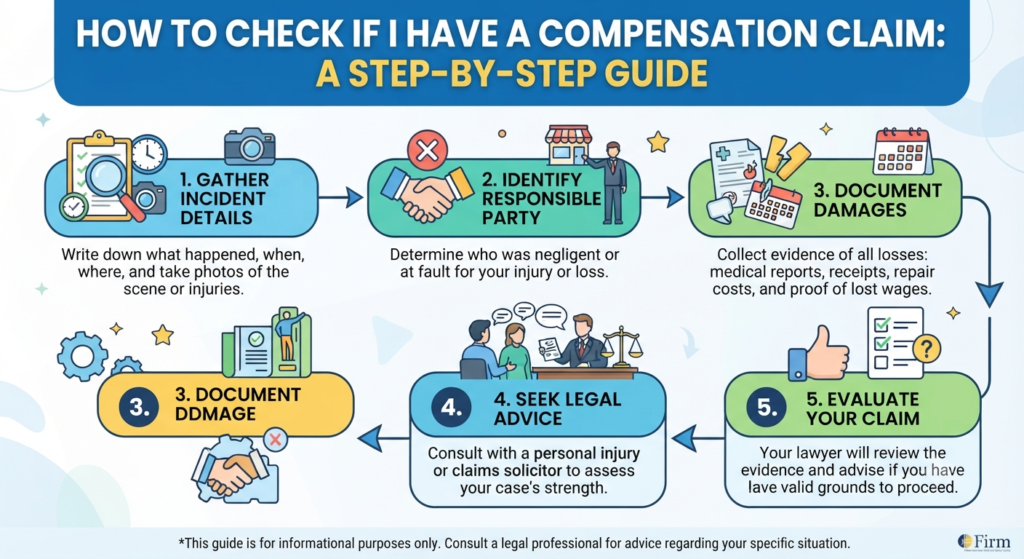

Practical Steps to Verify Your Claim

Before you contact a lawyer or file a formal complaint, follow these steps to build your “evidence foundation.”

- Document Everything Immediately: Memory fades and scenes are cleaned up. Take photos, record videos, and write down a detailed narrative while the events are fresh. If there were witnesses, get their contact information.

- Gather Official Records: Your word is rarely enough. Collect police reports, medical records, incident logs, or correspondence with the party you believe is at fault.

- Review Contracts and Insurance Policies: Sometimes, your right to compensation is defined by a contract. Read the fine print to see if the incident is specifically covered.

- Consult the “Statute of Limitations”: Every jurisdiction has a time limit for filing claims. Check your local laws immediately via the Legal Information Institute (LII) to see how much time you have.

When You Should Seek Professional Legal Help

Not all claims require an attorney, but some are too complex to handle alone. You should seriously consider professional representation if:

- Injuries are severe or long-term: Estimating future costs is complex and requires expert calculation according to standard medical accounting practices.

- Liability is disputed: If the other party denies fault or blames you, you will need skilled advocacy to combat a potential auto insurance claim denial.

- High-Value Claims: Insurance companies are trained to minimize payouts in large claims. Knowing how insurers calculate claim settlement amounts puts you in a much stronger position to negotiate.

- Complexity: Navigating intricate regulations is difficult for an average person to master under pressure. You can review consumer protection guidelines on the Federal Trade Commission (FTC) website to learn more about your rights against unfair practices.

Red Flags: Warning Signs of a Weak Claim

Avoid wasting time and resources on a claim that will likely be denied. Be honest about these factors:

- Lack of Evidence: If it’s purely your word against theirs with no physical proof, the case is weak.

- Pre-existing Conditions: If medical records show you had the same injury years ago, insurers will likely deny the claim.

- Failure to Mitigate: You have a duty to minimize your own losses. If you ignored medical advice or failed to secure damaged property, you might be held partially responsible.

Final Checklist Before You Proceed

Before you reach out to a claims adjuster or legal firm, answer these questions:

- [ ] Is there clear evidence of negligence by another party?

- [ ] Can I clearly quantify my financial and physical losses?

- [ ] Am I within the legal time limit (statute of limitations) to file?

- [ ] Have I gathered all available documentation (photos, reports, receipts)?

If you can confidently answer “yes” to these, you have a solid starting point for your claim. If you are still unsure, keep documenting and consult with a professional who understands how to negotiate settlements.

Disclaimer: This guide is for informational purposes only and does not constitute legal advice. Laws vary by region and individual circumstances; always consult with a qualified professional regarding your specific situation.