General Liability vs Professional Liability: The Ultimate Insurance Guide

In the modern business environment of 2026, the complexity of operations has increased significantly. Whether you are a solo consultant, a creative agency, or a brick-and-mortar retail business, managing risk is the foundation of long-term success. A common point of confusion for many entrepreneurs is understanding the distinction between General Liability vs Professional Liability. While both are types of commercial insurance, they protect against vastly different perils. Failure to understand these differences can lead to devastating coverage gaps that threaten your company’s survival.

Table of Content

- What is General Liability Insurance?

- Understanding Professional Liability Insurance (E&O)

- General Liability vs Professional Liability: The Core Differences

- Deep Dive into Industry-Specific Risks

- The “Silent” Risks: Why You Might Need Both

- Common Misconceptions in Business Insurance

- How to Assess Your Business Coverage Needs

- Best Practices for Claims Management

- Conclusion: Future-Proofing Your Business

What is General Liability Insurance?

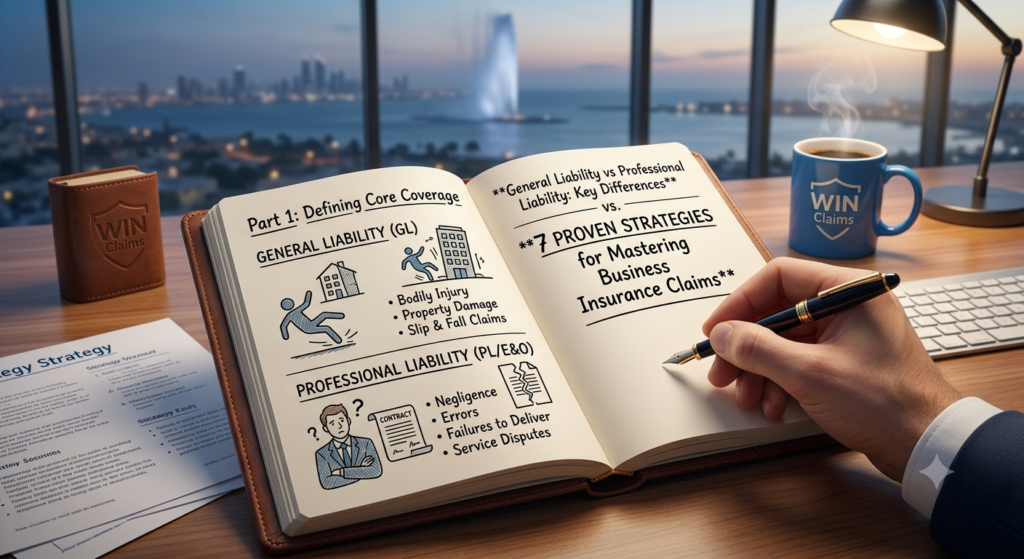

General Liability (GL) insurance is often viewed as the “safety net” of the business world. It covers common, accidental risks that can happen to almost any company. GL typically addresses three primary areas:

- Bodily Injury: If a client or a delivery person visits your office and slips on a wet floor, your GL policy covers their medical expenses and your legal defense costs.

- Property Damage: If you are working on a client’s premises and accidentally knock over an expensive piece of equipment, GL insurance covers the replacement or repair costs.

- Personal and Advertising Injury: This covers claims of slander, libel, or copyright infringement occurring during your advertising or business activities.

Understanding Professional Liability Insurance (E&O)

Professional Liability, frequently called Errors and Omissions (E&O) insurance, is far more specialized. It does not focus on physical accidents, but rather on the professional services you deliver. If a client accuses your firm of professional negligence, making a costly mistake, or failing to deliver the services outlined in your contract, this insurance provides the protection you need. It covers legal fees, settlements, and judgments, ensuring that a single project failure does not result in total bankruptcy.

General Liability vs Professional Liability: The Core Differences

To master the General Liability vs Professional Liability distinction, one must look at the nature of the damage. GL is about physical harm or tangible property damage. Professional Liability is about financial loss or loss of reputation stemming from your intellectual output or professional advice.

| Feature | General Liability | Professional Liability |

| Primary Focus | Physical & Tangible Risks | Intellectual & Financial Risks |

| Typical Claim | Injury on premises, property damage | Negligence, bad advice, service errors |

| Coverage Goal | Protecting the physical site | Protecting the service quality |

| Essential For | Retailers, Contractors, Offices | Consultants, Lawyers, Agencies |

Deep Dive into Industry-Specific Risks

Every industry carries a unique risk profile. A construction firm, for example, faces immense General Liability risks. They operate heavy machinery, create potential hazards on worksites, and often have third parties moving through their zones of operation. The likelihood of a physical accident here is high, making robust GL coverage non-negotiable.

On the other hand, consider a financial planning firm or a software developer. Their physical office space might be very safe, resulting in a lower GL risk. However, their Professional Liability exposure is massive. A faulty software update that deletes a client’s database or bad financial advice that leads to a loss of capital could trigger lawsuits worth millions of dollars. The risk is intangible, but the financial impact is absolute.

The “Silent” Risks: Why You Might Need Both

Many business owners make the critical mistake of choosing one policy over the other based on price. However, true risk management requires a holistic approach. Consider a consultant who meets a client at their office:

- They could trip and injure someone (GL claim).

- They could provide bad advice during that same meeting that causes the client to lose money (Professional Liability claim).

Relying on one policy leaves you exposed. Furthermore, many contracts in 2026 now require proof of both coverages before you can even bid on a project. Lacking one can effectively lock you out of high-value deals.

Common Misconceptions in Business Insurance

A major misconception is that Professional Liability is only for “high-level” professionals like doctors or lawyers. In reality, any business that provides a service, design, or specialized expertise needs E&O. Another misconception is that your business structure (LLC or Corporation) provides enough protection. While business entities offer some protection for personal assets, they do not pay for your legal defense or court judgments in the event of a lawsuit.

How to Assess Your Business Coverage Needs

To determine the right coverage, conduct a “Risk Audit”:

- Operational Audit: How much time do you spend on client sites? (Higher site time = more GL).

- Service Audit: Do you provide advice, designs, or technical solutions? (More advice = more Professional Liability).

- Asset Audit: How much liquid cash can your business afford to lose in a lawsuit? If the answer is “not much,” you need higher coverage limits.

Best Practices for Claims Management

When a claim occurs, speed and precision are paramount. Always report incidents immediately to your insurer. Keep detailed records of every interaction with your clients, including emails, contract versions, and notes from meetings. If a dispute escalates, professional advocacy is crucial. At WIN Claims, we advocate for business owners to ensure that the insurance company fulfills their contractual obligations properly, maximizing your potential recovery.

Conclusion: Future-Proofing Your Business

Understanding the General Liability vs Professional Liability dynamic is a fundamental step toward professional maturity. In 2026, the marketplace is unforgiving of those who leave their digital and physical assets unprotected. By investing in comprehensive insurance, you are not just paying for a policy; you are paying for the peace of mind that allows you to innovate, grow, and take the calculated risks necessary for true business success. Review your policies today—your business future depends on it.