1. Understanding the Auto Insurance Landscape in 2026

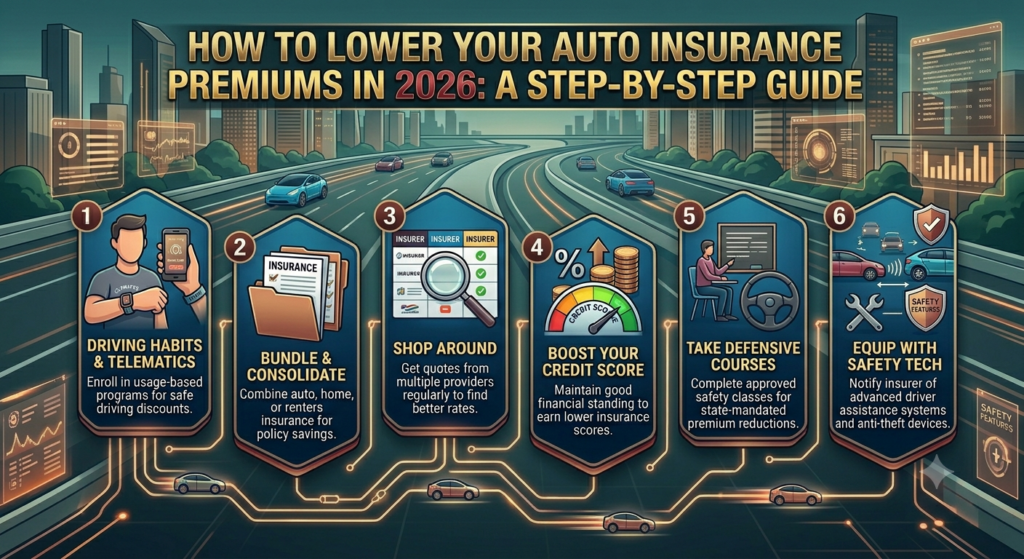

The automotive insurance industry has undergone a radical transformation by 2026, driven largely by the integration of artificial intelligence, real-time data analytics, and the widespread adoption of electric and autonomous vehicles. In previous years, premiums were largely calculated based on historical demographic data and static risk assessments. However, the current landscape has shifted toward dynamic, usage-based modeling. Insurers now leverage vast arrays of data points, including vehicle connectivity metrics, driving behavior patterns, and even real-time traffic density information. For the modern driver, understanding this landscape is not just about choosing the cheapest provider; it is about recognizing that your “risk profile” is a living, breathing set of data that changes with your every decision. If you want to lower your premiums, you must move from a passive consumer to an active participant in your insurance profile. To keep your costs low, you need to align your driving habits with the metrics that modern insurers value most: reliability, safety, and consistent compliance with traffic laws. For a deeper look at industry-wide regulations and consumer protection trends, you should regularly consult the official resources provided by the National Association of Insurance Commissioners (NAIC).

2. The Direct Impact of Credit Scores on Your Financial Security

It is a common misconception that auto insurance premiums are based solely on your driving record and the make of your car. In the vast majority of U.S. states, your credit-based insurance score is one of the most heavily weighted factors in determining what you pay each month. Insurance companies rely on actuarial studies that have historically shown a strong statistical correlation between how an individual manages their credit and their likelihood of filing a claim. In 2026, with financial volatility still a concern for many, maintaining a high credit score is essentially an insurance discount strategy. When your credit score drops, insurers perceive you as a higher risk, assuming that a lack of financial stability may lead you to cut corners on vehicle maintenance or file frivolous claims to recoup funds. To lower your premiums, you must treat your credit score with the same level of priority you give to your driving record. When you improve your creditworthiness, you aren’t just improving your ability to get a loan or a mortgage; you are actively lowering your monthly operating costs for your vehicle.

3. Comparing Quotes: Why Market Research is Your Greatest Asset

In the era of instant digital connectivity, there is absolutely no excuse for remaining with an insurance provider simply out of habit. Many drivers fall into the trap of “loyalty complacency,” assuming that staying with a carrier for years guarantees the best rates. In reality, the insurance market is hyper-competitive, and new customer discounts are often much more aggressive than renewal offers. In 2026, the most successful strategy for lowering your auto insurance premiums is to perform a systematic market comparison at least once every six months, or at the very least, prior to every policy renewal. However, not all comparison tools are created equal. You should rely on independent, third-party evaluations that provide unbiased reliability data rather than just price-focused aggregators. A primary resource for this type of due diligence is Consumer Reports, which offers extensive, data-backed reviews of both vehicle reliability and insurer performance. By cross-referencing your quotes with independent ratings, you ensure that you aren’t just buying the cheapest policy, but the most reliable one.

4. Bundling Policies: A Strategy for Savings

Consolidating your insurance needs under a single carrier is a classic but highly effective strategy. When you bundle your auto insurance with home, renters, or life insurance, providers often offer a significant multi-policy discount. This serves two purposes: it lowers your overall insurance spend and simplifies your financial management. Insurers prioritize “bundled” clients because they are statistically less likely to switch carriers, making you a more valuable asset to them in the long term.

5. Adjusting Your Deductibles Wisely

Your deductible—the amount you pay out-of-pocket before insurance kicks in—is inversely proportional to your premium. If you have an emergency fund capable of covering a higher repair bill, raising your deductible from $500 to $1,000 or $2,000 can result in immediate, significant savings on your annual premium. It is a calculated financial risk, but for many drivers, the math heavily favors higher deductibles over time.

6. Taking Defensive Driving Courses

Many states and individual insurers offer credits for drivers who complete certified defensive driving courses. These courses are designed to sharpen your hazard detection skills and improve overall safety. For high-risk demographics, such as young drivers or those with past moving violations, this can be the most effective way to rehabilitate their reputation with the insurance company.

7. Enrolling in Telematics and Usage-Based Insurance (UBI)

In 2026, “Usage-Based Insurance” is the standard for tech-savvy drivers. By allowing your insurer to track your driving habits—such as speed, braking, and time of day—through an app or device, you can receive personalized discounts. If you drive carefully and stick to predictable hours, your premium could drop by as much as 25% or more compared to traditional, non-UBI plans.

8. The Criticality of Continuous Coverage

Insurance companies penalize drivers for any “gap” in coverage. Even if you don’t own a car, purchasing a “non-owner” liability policy can keep your insurance history “continuous.” This is crucial because a lapse in coverage creates a red flag that marks you as high-risk, leading to much higher premiums when you eventually reinstate your full coverage.

9. Leveraging Advanced Vehicle Safety Features

Modern vehicles are packed with safety technologies, from blind-spot detection to autonomous braking. Insurance companies calculate premiums based on the likelihood of an accident occurring. If your car has these features, ensure your agent has filed them correctly in your profile. These technologies demonstrably reduce accident frequency, and insurers are often happy to provide credits for them.

10. Reporting Accurate Annual Mileage

In the era of hybrid work and telecommuting, many drivers are on the road less than they were years ago. Insurers charge based on risk, and risk is directly proportional to the time you spend on the road. If your commute has been reduced or eliminated, update your annual mileage estimates with your insurer immediately to see an instant adjustment in your rate.

11. Geographic Factors and Relocation Impacts

Your zip code is a major component of your insurance risk score. Factors like theft rates, accident frequency, and repair costs vary wildly by location. If you are planning to move, consider the insurance implications of your new location before settling on a final decision. Even moving a few miles can sometimes make a significant difference.

12. Removing Full Coverage from Older Vehicles

If you drive an older vehicle with low market value, continuing to pay for full coverage (comprehensive and collision) might be throwing money away. If the cost of the premiums over a few years exceeds the car’s actual cash value, it is often wise to drop those coverages and rely on liability-only protection.

13. Negotiating Tenure and Loyalty Credits

While loyalty complacency is bad, “tenure awareness” is good. Some insurers offer longevity discounts that aren’t advertised. After a few years with a carrier, call your agent and ask: “Are there any tenure-based credits available that I am not currently receiving?” You would be surprised how often this simple question works.

14. Utilizing Professional Association Discounts

Many insurance companies have partnerships with professional associations, unions, and alumni groups. Whether it is an engineering society, a teachers’ union, or a university alumni group, these organizations often negotiate exclusive group rates for their members. Check your affiliations today.

15. The Benefits of Annual Premium Payments

Paying your premium in a lump sum annually—rather than monthly—avoids installment fees and administrative charges. Many insurers offer an “in-full” discount, which can save you a percentage of the total premium. It is a simple financial maneuver that yields a guaranteed return.

16. Maintaining a Clean Motor Vehicle Report (MVR)

Your MVR is the official document of your driving history. Periodically request a copy of your own MVR to ensure there are no errors or old violations that should have already expired. If you find an error, challenge it through the DMV; cleaning your report is a direct route to lowering your premiums.

17. Avoiding Small, Frivolous Claims

Small claims are the enemy of low premiums. If you have a minor fender bender with minimal damage, it is often more cost-effective to pay for the repair out of pocket than to file a claim. Filing a claim can lead to a “surcharge” on your policy that lasts for years, costing you much more than the original repair.

18. Rehabilitating a “High-Risk” Status

If you currently hold a high-risk label due to past accidents or tickets, the best strategy is long-term rehabilitation. Maintain a clean record for 3 to 5 years, and then proactively contact your insurer to request a review of your risk profile. Most negative marks fade from your record, and you should demand that your rates reflect your current, improved behavior.

19. Adjusting Policy Based on Life Milestones

Life events like marriage, retirement, or moving into a new age bracket can change your insurance risk profile. For example, getting married often lowers your premiums as you are viewed as more stable. Always update your insurance provider about significant life changes.

20. Embracing Paperless and Automated Billing

Insurers love efficiency. Signing up for paperless statements and automatic electronic payments often qualifies you for small but recurring discounts. Over time, these add up, and they also prevent accidental missed payments that could lead to policy cancellations.

21. Eliminating Unnecessary Add-ons

Review your policy declarations page. Are you paying for roadside assistance, rental car reimbursement, or gap insurance that you no longer need? If you have an alternative service for roadside help or if your car is older, stripping away these extra add-ons can reduce your monthly bill.

22. Monitoring Credit for Unauthorized Entries

Beyond just having a high credit score, you must ensure your credit report is accurate. Identity theft or clerical errors can result in false marks that harm your insurance score. Use free annual credit report services to verify that all data is correct.

23. Working with Independent Insurance Brokers

Unlike “captive” agents who only sell for one company, independent brokers have access to policies from dozens of insurers. They can shop the market for you, saving you hours of time and ensuring you are placed with a carrier that offers the best value for your specific profile.

24. Coordinating Insurance with Other Assets

If you have significant assets, you might consider an umbrella policy, but always ensure that your underlying auto limits are set correctly. Sometimes, increasing liability limits is surprisingly cheap and can allow you to restructure your entire insurance portfolio for better efficiency.

25. Understanding State-Specific Minimums

Every state has different requirements for minimum liability coverage. While it is dangerous to be under-insured, it is also a waste of money to carry massive limits if you do not have significant assets to protect. Find the “sweet spot” that satisfies your state while keeping costs manageable.

26. Avoiding Aftermarket Modifications

While car modifications are fun, they are often a nightmare for insurance. Many insurers increase premiums significantly for modified vehicles due to the difficulty and cost of replacing aftermarket parts. If your goal is low insurance, keep your vehicle as close to stock as possible.

27. Installing Anti-Theft and Tracking Devices

If you park in an area with a high theft rate, installing a modern GPS tracking or anti-theft system can qualify you for comprehensive coverage discounts. Verify with your insurer which systems they approve before making an investment.

28. Balancing Liability Limits with Asset Protection

Your liability coverage should roughly match your net worth. If your insurance limits far exceed your total assets, you are essentially over-insuring. Regularly audit your net worth and adjust your liability limits accordingly to keep premiums in line with your actual financial risk.

29. Consistency and Patience

Insurance rates are rarely “fixed” forever; they fluctuate based on market cycles. The best strategy is to be a consistent, safe driver who audits their policy annually. By staying the course and avoiding “high-risk” behaviors, you naturally gravitate toward the lowest possible premium tiers over time.

30. Conducting an Annual Insurance Audit

Make it a yearly habit to perform a comprehensive “insurance audit.” Sit down with your policy, your credit report, and a list of your current driving needs. By proactively managing these factors every 12 months, you ensure you never pay a dollar more than necessary in an ever-changing insurance market.